Excessively withheld personal income tax posting. Personal income tax: we return, withhold, transfer. When can over-withheld personal income tax be offset?

E.A. answered questions. Sharonova, economist

Personal income tax: we return, withhold, transfer

Errors in calculating personal income tax are very unpleasant; there is too much hassle in correcting them. But the most annoying thing is that even if you yourself identify the error, pay additional tax and penalties and submit updated 2-NDFL certificates (new ones with correct data) to the Federal Tax Service, then, according to the regulatory authorities, this will not exempt you from the fine. And all because the rules of Art. 81 NKs do not work here. After all, an updated 2-NDFL certificate is not an updated calculation and not an updated declaration. True, there is a single court decision in which it stated the following. If the tax agent, before the start of the on-site tax audit, paid additional personal income tax and submitted the correct 2-NDFL certificate, then the conditions for exemption from the fine are met. Resolution of the FAS ZSO dated September 30, 2013 No. A27-17110/2012. But, as you yourself understand, you will most likely have to resolve this issue through the courts.

Now let’s see how organizations should act when identifying errors in personal income tax.

Salary is accrued in the month the error is discovered

A. Kiseleva, Belgorod

In April, I discovered that for February one employee’s salary was incorrectly calculated and accrued - less than necessary. And accordingly, personal income tax was underpaid. How can we now correct the situation so as not to pay fines and penalties?

: Despite the fact that the employee did not receive his salary in February, it is recognized as income in the month of additional accrual - in April clause 2 art. 223 Tax Code of the Russian Federation. An employee of the Ministry of Finance also agrees with this.

FROM AUTHENTIC SOURCES

Advisor to the State Civil Service of the Russian Federation, 1st class

“ Since the organization accrues additional income in the form of wages in April, that is, in the month the error was discovered, the additional accrued amount is April income. Consequently, the organization calculates personal income tax on this income in April clause 3 art. 226 Tax Code of the Russian Federation. The organization must withhold personal income tax from the April salary at the time of its payment. clause 4 art. 226 Tax Code of the Russian Federation. And transfer to the budget no later than the day you receive cash from the bank for its payments clause 6 art. 226 Tax Code of the Russian Federation.

Therefore, if an organization transfers personal income tax to the budget within this period, it will not face any fines or penalties. After all, there will be no reason for this.

An offense for which a fine is provided under Art. 123 of the Tax Code of the Russian Federation, can be imputed to a tax agent only if he had the opportunity to withhold and transfer the appropriate amount, taking into account the fact that the withholding is carried out from funds paid to the taxpayer in clause 21 of the Resolution of the Plenum of the Supreme Arbitration Court of July 30, 2013 No. 57” .

You must return the over-withheld personal income tax even to a former employee

G. Zalukaeva, St. Petersburg

The employee's personal income tax was withheld unnecessarily and transferred to the budget. We cannot refund the tax because the employee has already quit. What to do now with the amount of overpaid tax?

: First of all, within 10 days from the day you discovered excessive personal income tax withholding, you are obliged to inform your former employee about this clause 1 art. 231 Tax Code of the Russian Federation. You can send him a registered letter with return receipt requested to the address that he indicated to you when applying for a job.

If an employee comes to you and asks you to return over-withheld tax, you will be required to do so. clause 1 art. 231 Tax Code of the Russian Federation. As the Ministry of Finance explains, the dismissal of an employee, as well as the period in which the over-withheld tax is refunded, do not in any way affect this duty of the tax agent. Letter of the Ministry of Finance dated December 24, 2012 No. 03-04-05/6-1430.

ATTENTION

You cannot return personal income tax in cash from the cash register. At the same time, liability for the “cash” return of the Tax Code has not been established.

And this year the Constitutional Court agreed with the Ministry of Finance. He pointed out that the Tax Code of the Russian Federation provides for a special (special) procedure for the return of personal income tax over-withheld by a tax agent, which has priority over the general procedure for the return of tax overpayments Determination of the Constitutional Court dated February 17, 2015 No. 262-O. This means that a person cannot apply directly to the Federal Tax Service for a refund of the overpayment, bypassing the tax agent. A citizen can submit an application for the return of excessively withheld personal income tax along with the 3-NDFL declaration directly to the Federal Tax Service only if the tax agent is absent (for example, when it was liquidated) clause 1 art. 231 Tax Code of the Russian Federation.

So you will need to return the overly withheld tax to the employee, regardless of when he contacted you - before submitting the 2-NDFL certificate to the inspectorate or after.

When the employee comes to you, ask him to write a statement in which he must indicate the amount of personal income tax to be returned, the account number and bank details where the money should be transferred. You will have to return the tax within 3 months from the date of receipt of the application. At the same time, by the amount of tax returned to the former employee, you will reduce the amount of personal income tax to be transferred to the budget for other employees. clause 1 art. 231 Tax Code of the Russian Federation.

If the former employee does not show up by the end of the year, then at the end of the year, no later than 04/01/2016, you will submit a 2-NDFL certificate to the Federal Tax Service, where in clause 5.6 you will indicate the amount of excess tax withheld. clause 2 art. 230 Tax Code of the Russian Federation.

And if an employee comes to you after submitting a 2-NDFL certificate for him, then after the tax refund you will have to submit a new (clarifying) 2-NDFL certificate to the Federal Tax Service. In it you will reflect the correct data: on income, deductions, calculated (clause 5.3 of the certificate), withheld (clause 5.4 of the certificate) and transferred (clause 5.5 of the certificate) personal income tax. This certificate will no longer contain excessively withheld tax (clause 5.6 is not completed), and the amounts of personal income tax calculated, withheld and transferred will be equal. Keep in mind that this certificate must indicate the number of the previously submitted 2-NDFL certificate, but the date of preparation - the new one section I Recommendations, approved. By Order of the Federal Tax Service dated November 17, 2010 No. ММВ-7-3/611@ (hereinafter referred to as Order No. ММВ-7-3/611@).

You are required to withhold personal income tax from a working employee

L. Suhoveeva, Moscow

I came to the organization as chief accountant and discovered that an employee was mistakenly provided with a deduction for a child who was already over 30 years old. Probably, the previous accountant entered data taken from the air; there are no documents. When I informed the employee about this, he was indignant and refused to voluntarily return the tax, saying that if I wanted to, I could do it only through the court.

As far as I know, I cannot withhold personal income tax for past periods. Or is it still possible? Do I need to report it to the tax office?

: Actually, your employee is wrong about the court. In ch. 23 of the Tax Code directly states that tax amounts not withheld from employees or not fully withheld are collected from them by the organization itself until the debt is fully repaid and clause 2 art. 231 Tax Code of the Russian Federation. So you simply have to recalculate personal income tax and withhold it from the employee.

Another question is over what period this should be done. When conducting an on-site audit, tax officials have the right to inspect only 3 years preceding the year in which the decision to conduct audits was made and clause 4 art. 89 Tax Code of the Russian Federation. And when they will come to you is unknown.

In this situation, you can recalculate personal income tax for the 3 years preceding the year the error was discovered - 2012, 2013, 2014. As we understand, the error was discovered after submitting 2-NDFL certificates for this employee to the Federal Tax Service. Therefore you need to do this:

- recalculate the tax. If we assume that the employee was provided with an extra child deduction in the amount of 1,400 rubles every month for 3 years, then the total amount of excess deductions will be 50,400 rubles. (12 months x 3 years x 1400 rub.). And the personal income tax underwithheld from this amount will be equal to 6,552 rubles. (RUB 50,400 x 13%);

- inform the employee about the mistake made and the amount of personal income tax that must be withheld from him clause 2 art. 231 Tax Code of the Russian Federation;

- since the employee does not agree to repay the debt voluntarily, then withhold tax from the income paid to him. At the same time, the total amount of personal income tax withheld (tax for the current month + debt) should not exceed 50% of the amount given to the employee in person clause 4 art. 226 Tax Code of the Russian Federation;

- transfer the withheld tax to the budget;

- pay penalties to the budget for the period from the day following the day when personal income tax should have been transferred to the budget until the day of its actual payment, inclusive Art. 75 Tax Code of the Russian Federation;

- after you have withheld the entire personal income tax debt, submit to your Federal Tax Service newly compiled (clarifying) certificates 2-NDFL for this employee section I Recommendations, approved. By Order No. ММВ-7-3/611@. In them you will no longer have child deductions. And the amounts of calculated, withheld and transferred personal income tax will be greater. Moreover, all three personal income tax amounts in the certificates must be the same, since on the date of their submission the tax from the employee has already been withheld and transferred to the budget.

WE TELL THE EMPLOYEE

If an employee was provided with deductions to which he was not entitled, then the employer has the right to independently recalculate the personal income tax and withhold the underpaid amount of tax from the salary.

However, the fact that you submit updated 2-NDFL certificates to the Federal Tax Service and correct everything yourself before the tax authorities come to check you, unfortunately, will not save you from a fine for late transfer of personal income tax and penalties Articles 123, 75 of the Tax Code of the Russian Federation. After all, as the Ministry of Finance explained, exemption from a fine in this case is simply not provided for by the Tax Code Letter of the Ministry of Finance dated February 16, 2015 No. 03-02-07/1/6889. The only thing that can be done is to try to reduce the fine, citing the fact that your mitigating circumstances include correcting the error yourself and paying additional taxes and penalties. subp. 3 p. 1 art. 112 Tax Code of the Russian Federation. Maybe the inspectors will meet you halfway.

A former employee will not be able to withhold additional personal income tax

L. Kozhichkina, Bryansk

In March, when generating personal income tax reporting, I discovered an error: the amount of tax calculated turned out to be greater than the amount of tax withheld and transferred.

I started checking and discovered that for some reason the program did not calculate tax on the amount of sick leave for an employee, which we paid in October. This employee quit in September, and then gave us sick leave in October. Therefore, we cannot withhold personal income tax.

What to do now, what to reflect in the 2-NDFL certificate? What do we face - a fine or just penalties? Until when will penalties be accrued?

: Indeed, this is an unfortunate mistake. But its consequences are even sadder.

Firstly, you had the opportunity to withhold personal income tax when paying benefits, but did not do so. And accordingly, the tax was not transferred to the budget on time. Even though this was a program error, you still face a fine of 20% of the unwithheld personal income tax amount Art. 123 Tax Code of the Russian Federation.

Secondly, since after paying for sick leave, you no longer paid any amounts to the former employee until the end of the year, no later than 02/02/2015 (January 31 is a day off, Saturday) you had to inform your Federal Tax Service about the impossibility of withholding personal income tax clause 5 art. 226, paragraph 6 of Art. 6.1 Tax Code of the Russian Federation. That is, submit a 2-NDFL certificate for it with attribute “2”, where you had to indicate only income in the form of sick leave, as well as the amount calculated (clause 5.3 of the certificate) and non-withheld personal income tax (clause 5.7 of the certificate) pp. 1-3 Orders, approved. By Order of the Federal Tax Service dated September 16, 2011 No. ММВ-7-3/576@;. If you fail to submit the certificate within the prescribed period, you will face a fine of 200 rubles. clause 1 art. 126 Tax Code of the Russian Federation But this does not negate the obligation to present it. By the way, you must send the same certificate to your former employee. Since he will now have to declare the specified income and pay tax on it subp. 4 clause 1, pp. 2-4 tbsp. 228, paragraph 1, art. 229 Tax Code of the Russian Federation.

In addition, the Ministry of Finance and tax authorities believe that you must draw up a regular 2-NDFL certificate for this employee (with the sign “1”), which you submit to the Federal Tax Service no later than 04/01/2015 clause 2 art. 230 Tax Code of the Russian Federation; Letters of the Ministry of Finance dated December 29, 2011 No. 03-04-06/6-363; Federal Tax Service for Moscow dated 03/07/2014 No. 20-15/021334. It must reflect all calculations for the current year, namely all income received by him, all deductions provided, as well as the total amounts of personal income tax - calculated (clause 5.3 of the certificate), withheld (clause 5.4 of the certificate), transferred (clause 5.5 of the certificate) and unretained (clause 5.7 of the certificate) section II Recommendations, approved. By Order No. ММВ-7-3/611@.

Thirdly, for untimely transfer of personal income tax, you face penalties for the period from the moment when you were supposed to withhold and transfer the tax to the budget, and until the due date for its payment by an individual at the end of the tax period. clause 2 of the Resolution of the Plenum of the Supreme Arbitration Court of July 30, 2013 No. 57; Letter of the Federal Tax Service dated August 22, 2014 No. SA-4-7/16692. That is, penalties will have to be paid until July 15, 2015 inclusive clause 4 art. 228 Tax Code of the Russian Federation.

At the same time, you don’t have to pay fines and penalties, since the tax authorities themselves will collect everything from you if they come to check with you. Or maybe it will pass. In addition, when inspectors discover a violation, you can explain that personal income tax was not withheld on time not due to your fault, but due to a glitch in the program. And if the amount of the fine is large, then ask the tax authorities to reduce it, indicating that you yourself corrected the mistake subp. 3 p. 1 art. 112 Tax Code of the Russian Federation. It is possible that this will work.

Due to the transfer of personal income tax to the wrong KBK, fines and penalties are not threatened

M. Baryshnikov, Omsk

I am registered as an individual entrepreneur using the simplified procedure. And 10 months ago I registered as an employer. When registering with the Federal Tax Service, I was given a sample receipt for paying personal income tax for employees, which indicated the following BCC: 182 1 01 02030 01 1000 110. I paid the tax to it in a timely manner for 9 months, when I paid salaries to employees (residents of the Russian Federation).

In January 2015, I decided to clarify whether the BCC had changed since the new year. And I discovered that personal income tax for employees must be transferred to KBC 182 1 01 02010 01 1000 110. The same KBC was in effect in 2014.

It turns out that in 2014 I transferred personal income tax for employees using the wrong BCC. Is there any way to fix this now and what will I face (fines, penalties)?

: Indeed, you transferred personal income tax for your employees to the wrong KBK. After all, on KBK 182 1 01 020 30 01 1000 110 personal income tax must be paid in the case when individuals themselves declare their income in accordance with Art. 228 Tax Code of the Russian Federation Order of the Federal Tax Service dated December 30, 2014 No. ND-7-1/696@.

But, as a specialist from the Ministry of Finance explained, there is nothing wrong with this, everything can be fixed.

FROM AUTHENTIC SOURCES

“The Tax Code stipulates that if an error is detected in the execution of an order for the transfer of tax, which does not entail the non-transfer of this tax to the budget system of the Russian Federation to the appropriate account of the Federal Treasury, the taxpayer has the right to submit to the tax authority at the place of his registration a statement of the error with a request to clarify the basis, type and the nature of the payment, tax period or payer status. This application must be accompanied by documents confirming the payment by the taxpayer of the specified tax and its transfer to the budget system of the Russian Federation to the appropriate account of the Federal Treasury. clause 7 art. 45 Tax Code of the Russian Federation.

The procedure for clarifying the BCC can only be carried out within the same tax. In the case under consideration, this is possible, since the entrepreneur transferred personal income tax for employees to the wrong KBK, but also intended for this tax.

Based on the entrepreneur’s application, the tax authority will make a decision to clarify the payment, and will also recalculate (add) penalties automatically accrued to the tax amount Letters of the Ministry of Finance dated July 17, 2013 No. 03-02-07/2/27977; Federal Tax Service dated December 22, 2011 No. ZN-4-1/21889.

Now regarding the application of responsibility. Since the personal income tax was withheld by the entrepreneur and transferred in a timely manner and in full, the tax authority has no grounds for bringing him to tax liability under Art. 123 Tax Code of the Russian Federation.”

Advisor to the State Civil Service of the Russian Federation, 1st class

Good morning! Tell me how to properly return personal income tax in such a situation.

The employee is a father of many children. The place of work is basic, the salary is small. At the beginning of the year, the employee worked full time, then reduced time, then was on vacation for several months without saving his salary. During the period of work, the employee’s personal income tax was withheld as expected, with deductions provided. But when drawing up the 2-NDFL certificate, it turns out that the employee’s personal income tax was overdeducted (deductions for children for the months when the employee was on vacation without saving his salary were not covered by his salary from the beginning of the year), although in fact everything was withheld in a timely manner and clearly.

On the one hand: well, even if it is excessively withheld, we inform the employee, take his application, and transfer back the personal income tax. But on the other hand, according to the accounting data, this excessively withheld personal income tax does not exist, which means that it needs to be included in the accounting somehow? And how to do it? Or, in this case, does the employee return personal income tax through the Federal Tax Service?

Visual calculation of personal income tax in the table in the attachment.

Possible options for returning to an employee the personal income tax that was excessively withheld from him

The most common situation when an employee may overpay personal income tax during the year is when he submits to the employer, along with a notice issued by the tax office, an application for the return of withheld personal income tax in connection with the provision of a property deduction for purchased housing (apartment, room, residential building or share in them). After all, many people want not to pay personal income tax immediately after purchasing an apartment.

This is more profitable and easier than waiting until the end of the year and submitting a declaration in form 3-NDFL and an application for a tax refund to the tax office at your place of residence.

At the same time, the organization’s accountant has a question: what is the procedure for returning tax already withheld during the year and how can this be done? Well, let's figure it out.

We recalculate the tax

STEP 1. Make sure that the notification of confirmation by the tax authority of the employee’s right to a property tax deduction correctly indicates all the details of your organization (name, INN, KPP), as well as the last name, first name, patronymic and passport details of your employee. If there are any errors in the data, ask the employee to bring the correct notice.

STEP 2. Transfer the amount of property deduction specified in the notification to the 1-NDFL tax card created for this employee. If you use the standard form 1-NDFL, then you need to add a new line “Property tax deduction” to section 3 of the employee’s card immediately after the line “Standard tax deductions”.

The notification indicates on separate lines the amount of deduction attributable to the cost of housing and the amount of deduction attributable to interest on targeted loans (credits) taken for the purchase of housing. If your employee brought a notice in which two amounts are indicated, then by adding them up, you will receive the total deduction amount, which must be transferred to the 1-NDFL card.

Note. If an employee is just starting to use the property deduction, then the notification may indicate the maximum amount of the deduction (excluding interest on targeted loans (credits)) of 1 million rubles. or 2 million rubles. - depends on when the right to deduction arose. And if the employee has already claimed a deduction in one of the previous years, then the notification will indicate the amount of the remaining unused deduction transferred to 2009. In any case, you have no control over the correctness of the amounts indicated in the notification.

STEP 3. Receive a free-form application from the employee to provide him with a property deduction and to return the over-withheld personal income tax.

STEP 4. In the month in which the employee brought the notice and application, recalculate the tax from the beginning of the calendar year. At the same time, in the month of granting the property deduction, in section 3 of the standard 1-NDFL card, in the line “Tax debt due to the tax agent,” you must indicate the amount of excess personal income tax withheld.

From this month forward, do not withhold personal income tax from the employee’s income. If the amount of the property deduction exceeds the employee’s annual income, then the tax will not have to be withheld until the end of the year.

If the amount of the deduction does not exceed the employee’s annual income, then from the month in which the amount of income calculated from the beginning of the year exceeds the amount of the deduction, personal income tax will have to be calculated and withheld (provided that all excessively withheld personal income tax was returned to the employee - see below) .

STEP 5. In accounting, reverse the amount of personal income tax previously withheld from the employee: Dt 70 “Settlements with personnel for wages” - Kt 68 “Calculations for taxes and fees”, subaccount “Settlements for personal income tax at a rate of 13%”.

We return the tax to the employee

The Tax Code of the Russian Federation does not define how much personal income tax must be returned to an employee if he has submitted an application to the employer for the return of excessively withheld personal income tax. Let's consider the possible options.

OPTION 1. We return the tax at the expense of current personal income tax payments for other employees

Since the tax withheld from the employee has already been transferred to the budget, you can return the tax to him using the amounts of personal income tax withheld in the current month from the income of other employees of the organization. That is, you reduce the personal income tax for the current month, subject to payment to the budget, by the amount of the employee’s overpayment. This way, you are essentially doing the credit yourself.

In this case, the amount of the refunded tax is reflected in section 3 of the standard 1-NDFL card on the line “Excessively withheld tax amount was returned by the tax agent” in the month in which the tax was returned to the employee (issued from the cash register, transferred to the salary card). And in accounting the following entries are made: Dt 70 - Kt 50 “Cashier”, 51 “Settlement accounts”.

Organizations use this option, justifying it by the fact that the payment of personal income tax is not personalized. After all, you transfer personal income tax to the budget in one payment for all employees. The amount of the transferred tax attributable to each employee is not reflected either in the 1-NDFL card, or in the 2-NDFL certificate, which is submitted annually to the tax authority, or in the personal income tax budget settlement card filled out by the Federal Tax Service for your organization as a tax agent. Please note that this card indicates only the total amount of personal income tax transferred by you for all employees. Moreover, this personal income tax amount is always listed as an overpayment. Tax accruals and penalties may appear only after the tax inspectorate conducts an on-site audit based on the decision. So even if you do not pay personal income tax for the current month, the arrears will not appear on the card.

Specialists from the Moscow Federal Tax Service have nothing against such a return.

You will not be able to return to the employee in the current month the entire amount of excess tax withheld from personal income tax amounts withheld in the current month from the income of other employees of the organization, only if they do not cover the amount of debt to the employee. In this case, you can return the tax using your own funds. After all, there is no responsibility for this. But since this is not profitable for the organization, it is better to return the remaining amount of over-withheld tax to the employee in the following months.

So, let's summarize the pros and cons of the first option.

(+) With this option, the employee immediately receives the over-withheld personal income tax. You do not need to contact the tax authority with a tax refund application.

(?) The Ministry of Finance is against the return to an employee of excessively withheld tax at the expense of the current personal income tax withheld from other employees (see details below), and it is possible that some tax inspectorates will take the position of a financial authority. But even if this happens, the tax office will not be able to make any claims against you, since:

- firstly, you returned to the employee the tax withheld in excess of him in connection with the provision of a property deduction to him on the basis of a notice issued by the tax office;

— secondly, there will be no arrears in personal income tax in the budget.

OPTION 2. We return the tax from the budget

The Ministry of Finance believes that it is impossible to return excessively withheld tax to an employee at the expense of the current personal income tax withheld from other employees. Moreover, the financial department indicated that since Art. 231 of the Tax Code of the Russian Federation, a special procedure for offset or refund by a tax agent of amounts of excessively withheld tax is not defined, then the general procedure for refund or offset established by Art. 78 Tax Code of the Russian Federation.

Let's imagine what this procedure will look like in practice.

STEP 1. Having received an application for a tax refund from an employee from whom personal income tax was excessively withheld, you do not return the tax to him. You submit an application to your tax office for a refund from the personal income tax budget that was excessively withheld from the employee. Attached to this application are copies of documents: the employee’s application for a tax refund, notices of granting him a property deduction, 1-NDFL card, which indicates the amount of debt held by the tax agent.

STEP 3. After receiving money from the budget into your current account, you will return the tax to the employee.

This tax refund procedure has both advantages and disadvantages.

(+) In this case, you will definitely not face any claims from the tax authorities.

(-) It is unknown how long an employee will wait for a personal income tax refund, since tax refunds from the budget to the organization’s current account can take a long time.

At the same time, an organization can return the over-withheld personal income tax to an employee without waiting for the tax inspectorate to transfer the money to its current account, since the Tax Code of the Russian Federation allows this. That is, the organization will return personal income tax to the employee at its own expense. But then the tax refund procedure will be slightly different.

STEP 1. Having received an application for a tax refund from an employee from whom personal income tax was overdeducted, you return the tax to him at your own expense.

STEP 2. You still continue to pay personal income tax withheld from other employees to the budget.

STEP 3. Submit an application to your tax office for a refund from the budget of the personal income tax that was excessively withheld from the employee, attaching all documents to it.

STEP 4. After receiving money from the budget to your current account, close the overpayment of tax listed in account 68.

Now let's see what are the pros and cons of such a return procedure.

(+) There will be no claims from the tax office. The employee quickly receives over-withheld personal income tax.

(-) You are diverting the organization’s money from circulation.

However, when applying option 2, it is not clear why the organization should continue to transfer personal income tax to the budget in anticipation of the return of money from the budget that needs to be returned to the employee.

OPTION 3. We offset the tax against the upcoming personal income tax payment by this employee

The Russian Ministry of Finance believes that excessively withheld tax can not only be returned directly to the employee, but also offset against upcoming personal income tax payments in accordance with Art. 78 Tax Code of the Russian Federation. Although clause 1 of Art. 231 of the Tax Code of the Russian Federation speaks specifically about tax refund to the employee.

However, in practice this option will only work if:

— the amount of property deduction does not exceed the amount of the employee’s annual income;

- the employee brought a notice from the tax office at the beginning of the year, that is, a small amount of personal income tax was withheld from his income, for example, for 1 or 2 months.

Let's see if option 3 is any good.

(+) In this case there will be no disputes with the tax office.

(-) The period for an employee to receive a deduction extends over several months throughout the year. In addition, option 3 cannot always be applied.

* * *

Taking into account the pros and cons we have given, choose the most convenient option for you to return personal income tax to an employee. The easiest option for you is to get your tax back using taxes from other employees for the current month. And the most “conflict-free” option is to offset the tax against upcoming payments for this employee.

———————————

Appendix to the Order of the Federal Tax Service of Russia dated December 7, 2004 N SAE-3-04/

subp. 2 clause 1, clause 3 art. 220 Tax Code of the Russian Federation

approved By order of the Ministry of Taxes and Taxes of Russia dated October 31, 2003 N BG-3-04/583; clause 1 art. 230 Tax Code of the Russian Federation

subp. 2 p. 1 art. 220 Tax Code of the Russian Federation

clause 1 art. 231 Tax Code of the Russian Federation; Letter of the Federal Tax Service of Russia dated 09/03/2008 N 3-5-04/; Letters of the Ministry of Finance of Russia dated 04/02/2007 N 03-04-06-01/103, dated 02/13/2007 N 03-04-06-01/35, dated 06/26/2006 N 03-05-01-04/188; Information messages of the Federal Tax Service of Russia from 04/06/2005, from 03/18/2005

clause 3 art. 210, paragraph 1, art. 224, paragraph 3 of Art. 226 Tax Code of the Russian Federation; Letters of the Ministry of Finance of Russia dated 04/02/2007 N 03-04-06-01/103, dated 02/13/2007 N 03-04-06-01/35, dated 06/26/2006 N 03-05-01-04/188; Information messages of the Federal Tax Service of Russia from 04/06/2005, from 03/18/2005

Chart of accounts and instructions for its use, approved. By Order of the Ministry of Finance of Russia dated October 31, 2000 N 94n

approved By Order of the Federal Tax Service of Russia dated October 13, 2006 N SAE-3-04/

clause 2 art. 230 Tax Code of the Russian Federation

clause 4 section VII, paragraph 1 section. IX Recommendations on the procedure for maintaining the “Settlements with the Budget” database in tax authorities, approved. By Order of the Federal Tax Service of Russia dated March 16, 2007 N MM-3-10/ (as amended on January 11, 2008)

Letter from the Federal Tax Service of Russia for Moscow dated November 29, 2007 N 28-11/113476

clause 1 art. 231, art. 78 Tax Code of the Russian Federation

pp. 6, 14 art. 78 Tax Code of the Russian Federation

Resolution of the Federal Antimonopoly Service of the Ural District dated July 22, 2008 N F09-5055/08-S2

Letter of the Ministry of Finance of Russia dated 04/03/2009 N 03-04-06-01/76

pp. 6, 14 art. 78 Tax Code of the Russian Federation

Letter of the Ministry of Finance of Russia dated January 19, 2009 N 03-04-06-01/3

Read the full text of the article in the journal "Glavnaya Ledger" N 09, 2009

Refund to an employee of the excessively withheld amount of personal income tax

Thank you for your answer, but I would like to clarify something to be completely sure. It turns out that I must return all personal income tax withheld from January to June 2014 to the employee? Despite the fact that the documents were provided in July.

Yes, that's right. If, as a result of recalculation of the tax base, an employee has an overpayment of personal income tax, the excess tax amount withheld can be returned. You can read more about the return procedure here: http://usn.1gl.ru/#/document/111/11396/?utm_source=www.26-2.ru&utm_medium=refer&utm_campaign=qa_innerlink?step=7&utm_source=www.26-2 .ru&utm_medium=refer&utm_campaign=qa_innerlink

1. Situation: from what period can an employee be provided with a standard personal income tax deduction. The employee has been working in the organization since the beginning of the year, but submitted an application for a deduction later

If the employee submitted an application within the current year, then provide deductions from the beginning of this period. Even if he declared his right to a deduction in the middle of the year.*

In the Tax Code there is no connection between the emergence of the right to deduction and the date of filing the application. There is also no time limit for when an employee must write such a statement. In this case, the deduction is due for each month of the calendar year until the employee loses the right to it. Therefore, if an employee has confirmed his right to a deduction since the beginning of the year (albeit in the middle), reduce his base for calculating personal income tax from January.

As you know, the base for personal income tax is calculated with each payment of income. This means that when paying, for example, wages for the month in which the employee confirmed his right, previously unaccounted deductions can be counted as a reduction in the tax base.

An example of calculating personal income tax if an employee applied for a deduction in the middle of the year

VC. Volkov has been working at ZAO Alfa since January 1 as a shop manager. His salary is set at 50,000 rubles. Volkov has three minor children. However, he did not immediately submit to the accounting department all the necessary documents to receive a standard tax deduction. Volkov did this only in July. Therefore, from January to June, when calculating personal income tax, Volkov was not provided with deductions.

In total, from January to June, Volkov was credited with 300,000 rubles. (RUB 50,000 × 6 months).

Personal income tax was withheld in the amount of 39,000 rubles. (RUB 300,000 × 13%).

The monthly deduction amount for three children is 5,800 rubles. (1400 rub. + 1400 rub. + 3000 rub.).

Starting from the month in which Volkov’s income exceeded 280,000 rubles, he has no right to a deduction. Volkov’s income reached its maximum in June. Therefore, when calculating personal income tax for January–July, the Alpha accountant provided Volkov with deductions for January–May.

The total deduction for five months is 29,000 rubles. (5800 rubles × 5 months).

The amount of excessively withheld personal income tax as of July 1 is:

39,000 rub. – ((300,000 rub. – 29,000 rub.) × 13%) = 3,770 rub.

The Alpha accountant counts this amount towards personal income tax, which must be withheld from Volkov’s salary for July.

The amount of personal income tax that needs to be transferred to the budget from Volkov’s income for January–July is equal to:

(350,000 rub. – 29,000 rub.) × 13% – 39,000 rub. = 2730 rub.*

All this follows from subparagraphs 1, 2 and 4 of paragraph 1 and paragraph 3 of Article 218 of the Tax Code of the Russian Federation. There are similar explanations in the letter of the Ministry of Finance of Russia dated April 18, 2012 No. 03-04-06/8-118.

In commercial organizations

If, as a result of recalculation of the tax base, an employee has an overpayment of personal income tax, the excess tax amount withheld can be returned.*

2. Article: Statement to "children's" deduction presented in December (edited for commercial organizations)

When should an employee submit an application to the accounting department for a standard tax deduction? What if it is filed at the end of the year? Experts from Zarplata magazine answer your questions.

The employee started working at the beginning of the year , A statement and documents for providing standard tax deduction I brought it for a child (a five-year-old son) only now - in December!

Tell me, please, what should we do? In this case, is it necessary to provide deduction at first of the year and recalculate personal income tax, or deduction is it available from the month of application?

A. Zimorod, accountant

Reasons for providing deduction . As a general rule, standard tax deductions for personal income tax are provided when taxing income taxed at a rate of 13% (clause 3 of Article 210 of the Tax Code of the Russian Federation) on the basis of (clause 3 of Article 218 of the Tax Code of the Russian Federation):

The legislation does not establish a deadline for providing these documents. Receiving a standard tax deduction is a right, not an obligation, of the taxpayer.

Cumulative total. Calculation of personal income tax amounts on income taxed at a rate of 13% is carried out at the end of each month on an accrual basis from the beginning of the year. In this case, the amount of personal income tax accrued from the beginning of the year is reduced by the amount of tax withheld in the previous months of the current year.

For personal income tax, the tax period is considered to be a calendar year (Article 216 of the Tax Code of the Russian Federation)

Right to recalculation. Now let's figure out whether the tax agent needs to recalculate personal income tax from the beginning of the year if the employee applied for a deduction in the middle or end of the year.

If the employee had the right to receive a deduction, but it was not provided due to the lack of an application and the necessary documents, the tax agent can recalculate the personal income tax amount.

To do this, the employee must:

- write a statement with a corresponding request for recalculation;

- Attach documents confirming the right to deduction to the application.

- from the income of the same person who had an overpayment (for example, if an employee from whom the excess amount of personal income tax was withheld continues to work in the organization);

- from the income of other taxpayers for whom the organization is a tax agent.*

- an extract from the tax register for personal income tax on the employee’s income;

- documents confirming the fact of excessive withholding and transfer of personal income tax.*

- a copy of the employee’s application (indicating the reason for the overpayment, the date of its occurrence and the amount);

- a copy of the certificate in form 2-NDFL as of the date of application for a refund;

- data on settlements with the budget for personal income tax starting from the year for which the tax was recalculated. As a document confirming the data on settlements with the budget for personal income tax, you can submit an extract from account 68 subaccount “Settlements with the budget for personal income tax.” The amount of accruals on the credit of this account must be reversed by the amount of the tax overpayment (so that the amount of the overpayment is visible).

Offset of excessively withheld personal income tax. The employer, who is a tax agent, is obliged to recalculate the tax and offset the excess withheld amount against the payment of the December personal income tax amount.

Refund of over-withheld personal income tax. If the amount of tax withheld in excess is greater than the amount of tax subject to withholding for December 2012, then, based on the employee’s application, the tax agent is obliged to return the difference to him in the manner prescribed by Article 231 of the Tax Code. In the application, the employee must indicate to which account this amount should be transferred.

There are still no documents. If by the end of the tax period the employee has not submitted an application for standard tax deductions to the accounting department or has not submitted a full package of documents necessary to receive a standard tax deduction, then the employer does not have the right to independently make a decision on recalculation and return of excessively withheld personal income tax.

In this case, recalculation and refund of tax in accordance with paragraph 4 of Article 218 of the Tax Code are carried out by the tax authority at the end of the tax period.

To do this, the employee must submit a tax return (form 3-NDFL) and documents confirming the right to the deduction to the tax office at his place of residence.*

Magazine "Salary", No. 12, December 2012

How can accounting entries reflect the payment to an employee and the amount of over-withheld personal income tax?

How can accounting entries reflect the payment to an employee of the amount of over-withheld personal income tax?

Refunds of over-withheld personal income tax are carried out only by bank transfer. In this case, previously incompletely paid wages are paid.

A detailed procedure for recording transactions for the return of amounts of excessively withheld personal income tax is contained in the materials of the Glavbukh System

Situation: An example of returning excessively withheld personal income tax to an employee at a rate of 13 percent. The overpayment is returned at the expense of upcoming personal income tax payments, subject to withholding and transfer to the budget from employee income

In August 2013, an employee of LLC Trading Company Hermes A.S. Kondratiev was on a business trip. Upon his return, he submitted an advance report in which he reflected the costs of travel to the place of business trip and back in the amount of 10,000 rubles. He did not have tickets confirming travel expenses.

Despite this, travel expenses were compensated to Kondratiev based on his application and the order of the manager. The accountant included the reimbursable expenses in the personal income tax base in August. The amount of personal income tax on compensation for travel expenses was 1,300 rubles.

Kondratyev’s monthly income is 8,000 rubles. Kondratiev has no children. For the period January–August, standard deductions were not provided to the employee. Data on accrued income and withheld tax are given in the table.

Period

Amount of taxable income

Mechanism for returning excessively withheld personal income tax from a dismissed employee

The organization unnecessarily withheld personal income tax from the employee. At the time the error was discovered, this employee quit and does not work in the organization. How do we notify the employee to write a statement and what will be the return mechanism?

Having discovered excessive withholding and overpayment of personal income tax, the employer must notify the employee about this within 10 days. The form and method of communication are not provided for by the Tax Code of the Russian Federation, therefore the tax agent has the right to send a message to the taxpayer in any form. To return excessively withheld personal income tax, a former employee must write a free-form application addressed to the manager. A former employee can file a tax refund application within three years from the date the excess amounts were withheld. You can return the money through upcoming personal income tax payments from the income of other employees. The organization must transfer the overpayment of personal income tax to the person’s bank account within three months from the date of receipt of the application from him. If upcoming personal income tax payments are not enough to refund the overly withheld tax amount within a three-month period, the tax agent should apply for a refund of the missing amount to the tax office. The tax refund application should be accompanied by: an extract from the personal income tax register on the employee’s income; documents confirming the fact of excessive withholding and transfer of personal income tax. Before the overpayment is credited to the organization's current account, the tax agent has the right to return the excessively withheld amount of personal income tax to the person at his own expense.

The rationale for this position is given below in the materials of the Glavbukh System

Refund of overpayment through the organization

For a refund of over-withheld personal income tax, a person can contact the organization that withheld the tax as a tax agent. To do this, he needs to write a statement in any form addressed to the head of the organization.* This is stated in paragraph 1 of Article 231 of the Tax Code of the Russian Federation.

A person can submit an application for a tax refund within three years from the date of its withholding* (Clause 7, Article 78 of the Tax Code of the Russian Federation). At the same time, the right to apply for a tax refund does not depend on the existence of labor (civil) relations between a person and an organization on the date of filing the application. For example, a person has the right to submit an application for the return of an excessively withheld amount to an organization after dismissal from it, but before the expiration of the period provided for a tax refund. In this case, the tax agent is obliged to return the excessively withheld personal income tax to the dismissed employee. In this case, confirmation that the tax was not returned by the tax inspectorate is not required.* Similar explanations are contained in letters of the Ministry of Finance of Russia dated December 27, 2012 No. 03-04-06/4-370 and dated December 24, 2012 No. 03- 04-05/6-1430.

Sources for the return of overpayments may be upcoming payments for personal income tax, withheld and subject to transfer to the budget:*

This follows from the provisions of paragraph 3 of paragraph 1 of Article 231 of the Tax Code of the Russian Federation.

The tax rates at which personal income tax was withheld, sent by the organization to return the overpayment, do not matter. For example, a tax calculated at a rate of 13 percent can be returned from personal income tax amounts calculated at rates of 9, 13, 30 or 35 percent. At the same time, tax agents are required to keep separate records of income (personal income tax amounts), for which different tax rates are applied (clause 3 of Article 226 of the Tax Code of the Russian Federation).

Return period

The organization must transfer the overpayment of personal income tax to the person’s bank account within three months from the date of receipt of his application.* There is no need to report the refund to the tax office (letter of the Ministry of Finance of Russia dated October 18, 2013 No. 03-04-06/43608). If within three months the organization does not return the overpayment to the taxpayer (in whole or in part), then it will have to charge interest on the amount of unrefunded tax for each day of delay. Interest is accrued at the refinancing rates in effect on the days the repayment deadline was missed. This procedure is provided for in paragraphs 3–5 of paragraph 1 of Article 231 of the Tax Code of the Russian Federation. In this case, the amount of accrued interest is not exempt from taxation. Such income is not mentioned in Article 217 of the Tax Code of the Russian Federation, therefore, when paying interest, personal income tax must be withheld from it. The validity of this conclusion is confirmed by the letter of the Ministry of Finance of Russia dated August 22, 2013 No. 03-04-05/34450.

The organization itself discovered the overpayment

If an organization-tax agent discovers an overpayment of personal income tax on its own, it is obliged to inform the taxpayer about this within 10 working days (paragraph 2, paragraph 1, article 231, paragraph 6, article 6.1 of the Tax Code of the Russian Federation). The Tax Code of the Russian Federation does not provide for the form and method of reporting the presence of an overpayment of personal income tax. Therefore, the tax agent has the right to send a message to the taxpayer in any form.* Such clarifications are contained in the letter of the Ministry of Finance of Russia dated May 16, 2011 No. 03-04-06/6-112.

Refund of overpayment through inspection

Upcoming personal income tax payments may not be enough to return the overly withheld tax amount within the three-month period established by paragraph 3 of paragraph 1 of Article 231 of the Tax Code of the Russian Federation. In this case, the tax agent should apply for a refund of the missing amount to the tax office at the place of his registration.

An application for the return of an excessively transferred amount of personal income tax must be submitted to the inspectorate within 10 working days from the date of receipt of the application from the taxpayer* (paragraph 6, paragraph 1, article 231, paragraph 6, article 6.1 of the Tax Code of the Russian Federation). Therefore, the tax agent must make a decision on the method of returning the overpayment (at the expense of upcoming payments or at the expense of funds returned by the inspection) immediately after receiving the taxpayer’s application* (letter of the Ministry of Finance of Russia dated May 16, 2011 No. 03-04-06/6-112) .

The tax inspectorate will return the overpayment of personal income tax to the tax agent organization in the manner established by Article 78 of the Tax Code of the Russian Federation* (paragraph 7, clause 1, article 231 of the Tax Code of the Russian Federation). Before the overpayment is credited to the organization's current account, the tax agent has the right to return the excessively withheld amount of personal income tax to the person at his own expense* (paragraph 9, clause 1, article 231 of the Tax Code of the Russian Federation).

If it is decided to return the overpayment using funds returned from the budget, a package of documents must be submitted to the tax office. The composition of this package does not depend on the type of income in respect of which an overpayment of personal income tax arose, and on the rate at which the tax was withheld* (letter of the Federal Tax Service of Russia dated September 20, 2013 No. BS-4-11/17025).

The tax refund application must be accompanied by:

The list of such documents is not established by law. However, in practice, the inspectorate may require the tax agent to:

Sergey Razgulin,

Actual State Councilor of the Russian Federation, 3rd class

2. Article: What to do if personal income tax needs to be returned to a former employee

What are the rules for returning taxes to fired employees?

If at the time when excessive withholding was discovered, the employee had already quit, the money can only be returned through upcoming personal income tax payments from the income of other employees.* This is exactly what the Russian Ministry of Finance says in its letter dated July 2, 2012 No. 03-04- 06/6-193.

note

A former employee can submit an application for a tax refund within three years from the moment when the excess amounts were withheld* (Clause 7, Article 78 of the Tax Code of the Russian Federation).

Moreover, a former employee can submit an application for a tax refund within three years from the moment when the corresponding amounts were withheld from him (Clause 7, Article 78 of the Tax Code of the Russian Federation). If the deadline is met, the former employer cannot refuse to return the personal income tax.

However, the situation is often complicated by the fact that the dismissed employee cannot personally come and write a return application. For example, he moved to another city. There is a way out of this. An accountant can send a sample application to a former employee by mail (both electronic and regular) or dictate by phone. And the employee will write it by hand and send it back by registered mail.

Example 2. Refund of personal income tax to a dismissed employee at the expense of upcoming tax payments from the salaries of other employees

Sales Manager of Zvezda LLC A.V. Rogov was fired on July 17 due to staff reduction. On July 26, the accountant discovered a technical error in calculating the tax on severance pay equal to 120,000 rubles. Instead of 15,600 rub. Personal income tax (120,000 rubles × 13%) was withheld 16,500 rubles. How to return to an employee excessively withheld personal income tax in the amount of 900 rubles. (RUB 16,500 – RUB 15,600)?

Immediately after discovering the error, the accountant called the dismissed employee and agreed with him on the procedure for returning the overpayment. By email to A.V. A message was sent to Rogov about the fact of excessive tax withholding, indicating the reason (technical error) and the amount of the overpayment - 900 rubles.* Attached to the letter was a sample application for the return of the overpayment. A.V. Rogov wrote a statement (see picture) indicating the details of his bank account to which the money should be transferred, and sent it to the organization by mail.

When paying employees remuneration for work in August, the accountant of Zvezda LLC withheld personal income tax in the amount of 70,000 rubles. And he paid 69,100 rubles to the budget. On the same day, personal income tax in the amount of 900 rubles was excessively withheld from the severance pay. was transferred to the bank account indicated by A.V. Rogov in a statement.

Useful tips

How to return personal income tax using funds that have already been paid to the budget

Sometimes upcoming personal income tax payments are not enough to receive a tax refund. This situation may arise, for example, during downtime, or the refund amount is very large due to what is owed to a top manager.

One way out is to return the overpayment in several stages. But this can only be done within a strictly allotted time - within three months from the date the employee submitted the application. If the deadline is violated, you will have to pay a penalty. Interest is accrued for each day of delay at the refinancing rate that was in effect on the days the repayment deadline was violated (clause 1 of Article 231 of the Tax Code of the Russian Federation).

If it is clear in advance that it will not be possible to meet the deadlines, there is only one way out - to ask the inspectorate to return the tax at the expense of the budget. Then the tax agent, no later than 10 days from the date of receipt of the employee’s application for a refund, also contacts the tax authorities with an application for a refund. It must be accompanied by documents confirming the excessive withholding of tax amounts - a copy of the employee’s application, a certificate in form 2-NDFL, a register of information on the income of individuals and payment documents for tax payment* (letter of the Ministry of Finance of Russia dated 04/03/2009 No. 03-04- 06-01/76). Please note that the list of documents is open and may change depending on the circumstances. The inspection will return the personal income tax to the organization's current account within one month from the date of receipt of the application from the company (Article 78 of the Tax Code of the Russian Federation). And then the tax agent will transfer the money to the employee himself.*

By the way, the Tax Code of the Russian Federation does not prohibit the return of overpayments at the expense of the company’s own funds. But we recommend doing this only if the organization is absolutely sure that the tax office will also return the money a little later. Otherwise, you may not get these funds back.*

The Ministry of Finance of Russia, in its letter dated July 2, 2012 No. 03-04-06/6-193, drew attention to another important circumstance. The personal income tax refund does not depend on the tax period in which the tax was excessively withheld. For example, an employee was fired at the end of 2011 and in the same year excess tax was paid. And the overpayment was discovered already in 2012. The employer has the right to return the money to the former employee in 2012 on a general basis. There are no special rules for this situation. The main thing is to ensure that the refund mechanism is launched immediately after the overpayment is detected.

Nuances requiring special attention

Having discovered excessive withholding and overpayment of personal income tax, the employer must notify the employee about this within 10 days.

The company has no right to refund taxes without a written application from the employee.

The tax overpayment can be returned through future personal income tax payments from both the employee’s salary and that of other employees. And if there is not enough money, then at the expense of funds previously paid to the budget.*

N.P. Epikhin,

expert of the magazine "Simplified"

* This is how part of the material is highlighted that will help you make the right decision

Postings in the 1C program when returning excessively withheld personal income tax

Questions and answers on the topic

In June 2017, an employee of the organization provided a Notification from the Federal Tax Service about the possibility of obtaining a property deduction through the employer. Over the past 5 months of this year, personal income tax has already been withheld from him and reports for the 1st quarter of 2017 have been submitted. When entering information about the employee’s property deduction into the 1C program, the accountant indicated the period for applying the deduction: 2017. Thus, when calculating wages and calculating personal income tax for the month of June 2017, the program recalculated personal income tax starting from January 1, 2017. In July, the employee was paid the required amount (entries similar to the payment of wages). What entries should the accountant use when paying the over-withheld tax? The question was asked due to the fact that in Section 1 of form 6-NDFL for 9 months of 2017, columns 070, 090 are filled out incorrectly.

Postings when returning excessively withheld personal income tax:

1) Reversal debit account 70 Credit account 68— reflects the amount of tax to be refunded. This is how you reduce the personal income tax that was previously withheld from the employee. As a result, the balance in the amount of recalculated tax will remain in account 70.

2) Since the balance of the tax hangs on account 70, you reflect the returned amount by posting:

Debit account 70 “Settlements with personnel for wages” Credit account 51“Current accounts” - reflects the amount of tax that you returned to the employee.

As a result, in the debit of account 68 you should see the amount of personal income tax from the property deduction, which you actually overpaid to the budget. By this amount you reduce your current tax payment.

If you returned the personal income tax to the employee in June, then reflect these changes on lines 030 and 090 of section 1 of the 6-NDFL calculation for the first half of 2017.

In line 030 put the increased deduction, in line 090 - personal income tax, which was recalculated. You do not reduce line 070 by personal income tax, which was returned to the employee. This is what the Federal Tax Service advises (Letter of the Federal Tax Service of Russia dated April 12, 2017 N BS-4-11/6925)

What does your program do? I can only assume that most likely she recalculates the calculated and withheld tax in lines 040 and 070, reducing this amount by the recalculated personal income tax, and the amount that you returned to the employee is not reflected in line 090. I can only advise correcting this data manually to bring them to the form recommended by the Federal Tax Service.

Calculation of personal income tax and refund of over-withheld tax to the employee

Question about personal income tax. The employee was on labor and employment leave in the middle of the year, then returned to work part-time. Deductions, according to the statement, are provided for two children. Below are the income, deductions and calculated personal income tax for the year: January - 23238.28-2800-2657 rubles. February - 23611.11-2800-2705 rub. March - 25000-2800-2886 rub. April - 25000-2800-2886 rub. May - 25000-2800-2886 rub. June - July - August - September - October - 1988.64-2800-0 rub. November - 6137.72-2800-434 rub. December - 6250-2800-448 rub. Apparently, the balance of the unused deduction in October (RUB 811.36) should have been transferred to November? This was not done. What are our actions now and how can all these amounts be reflected in the 2-NDFL certificate and in the 6-NDFL calculation?

Yes, you should have carried forward the balance of your unused deduction from October to November. In addition, the employee is also entitled to deductions for months in which there was no income - June, July, August and September, because the employment relationship with her was not interrupted, and income appeared at the end of the year (letters from the Ministry of Finance of Russia dated 09/04/2017 N 03-04 -06/56583 and Federal Tax Service of Russia dated May 29, 2015 N BS-19-11/112). Thus, you withheld extra tax in the amount of 1,561 rubles from the employee. (RUB 14,902 – RUB 13,341) (see table below).

You, as a tax agent, are obliged to return the overly withheld tax to the employee (Article 231 of the Tax Code of the Russian Federation). Your actions are as follows.

1. Notify the employee in writing that tax was over-withheld from her income in 2017. Do this within 10 working days from the day you discovered the error (letter from the Ministry of Finance dated May 16, 2011 No. 03-04-06/6-112).

2. Receive an application from the employee for the return of the excessively withheld amount of personal income tax, indicating the bank account details for transferring the money. You cannot return personal income tax in cash. The employee must submit such an application to you before the expiration of three years from the date of payment of the overly withheld tax to the budget (Letters of the Ministry of Finance dated January 20, 2017 N 03-04-06/2416, dated December 27, 2012 N 03-04-06/4-370). Sample below.

Example. An employee’s application for the return of excessively withheld personal income tax

General Director of Alpha LLC

from manager Petrova E.A.

I ask you to return to me the amount of personal income tax in the amount of 1,561 rubles, excessively withheld for 2017. I ask you to transfer the specified amount to a bank account opened for crediting wages.

3. Transfer the amount of over-withheld personal income tax to the account specified in the refund application. This must be done within three months from the date of receipt of the application (Letter of the Federal Tax Service dated July 18, 2016 N BS-4-11/).

4. By the amount of the refunded tax, reduce the amount of current personal income tax payments calculated from payments to all individuals who received income from you.

Now about how to fill out the 6-NDFL and 2-NDFL reports.

Annual 6-NDFL

In section 1, you will add to the indicator on line 020 the amount of the employee’s income - 136,225.75 rubles, on line 030 - the deductions provided to her - 33,600 rubles. In line 040 you will add the calculated personal income tax taking into account all deductions, that is, 13,341 rubles. ((RUB 136,225.75 – RUB 33,600 x 13%).

In line 070 you will show all personal income tax withheld in 2017, including excess personal income tax withheld from the employee’s income. That is, if you withheld tax from your December salary in December, include RUB 070 - 14,902 in line for the employee.

In line 090 of the annual form 6-NDFL, you do not reflect the returned tax of 1,561 rubles, since you did not return this amount in 2017.

In lines 140 of section 2, you will also reflect all personal income tax actually withheld when issuing wages, including excess amounts withheld.

6-NDFL for the first quarter of 2018

If you return the over-withheld tax no later than March 31, you will show this amount on line 090 of Form 6-NDFL for the 1st quarter of 2018. If you return it later, reflect this amount in line 090 of form 6-NDFL for the six months.

Help 2-NDFL

In section 3 of the certificate you will reflect all the employee’s income, in section 4 you will show deductions. And fill out section 5 like this:

FINE FOR A FOREIGNER WITHOUT PERMISSION FMS employees do not like this article. Since it provides for a “small” fine, only for the foreigner himself. And they are interested in imposing a “large” fine on a company that employs a foreigner without a work permit. Article 18.10. […] In a beauty salon, hairdressers work on a staggered schedule, and therefore do not complete the required number of working days. The actual number of craftsmen is 6 people, the average number (based on hours actually worked) is 4 people. From what number to produce [...]

Procedure for the return of overpaid personal income tax amounts

Note 1

The Tax Code of the Russian Federation, namely, Article 231, defines the procedure for returning excessively withheld personal income tax. The refund must be made by a tax agent. If there is no tax agent, the refund is carried out by the tax authority at the taxpayer’s place of registration.

Too much personal income tax withholding from a taxpayer’s income can be detected by both the taxpayer himself and the tax agent. If the fact of overpayment of personal income tax is discovered by a tax agent, he is obliged to inform the employee about it. This must be done within ten days from the day this fact was discovered.

The amount of personal income tax that was excessively withheld must be returned to the employee-taxpayer based on his written application.

It is also worth noting that the Tax Code does not indicate a clear form and method for informing an employee of the fact of excessive personal income tax withholding, as well as its amount. This suggests that this procedure can be carried out in any form.

The refund of the amount of over-withheld personal income tax is carried out within three months, starting from the day the tax agent received the corresponding application from the taxpayer. The refund must be made from the amounts of this tax that are subject to payment to the budget on account of future payments, both for this taxpayer and for other employee-taxpayers, from whose income the tax agent withholds this type of tax.

Note 2

Transfer of overpaid personal income tax amounts to an employee is carried out only in non-cash form.

Very often there are situations when the amount of personal income tax that is subject to transfer to the budget is not enough to refund the tax to the employee on time. In this case, the employer should apply for a tax refund to the tax office with an application for a refund of the excessively withheld tax amount.

Reflection of personal income tax returns in the 1C: Accounting program

If personal income tax was withheld from the employee in a larger amount, the program will report this. This can be seen by going to the “Payroll” document. By opening this document and going to the “Personal Income Tax” tab, you can see negative tax amounts.

In the same document, on the “Payment adjustments” tab, the amount to be offset is given. This occurs if the amount of income tax with a minus sign is greater than the amount of accrued tax for the current period.

After this document is completed, a posting will be generated: Dt 70 Kt 68.01, and the posting amount will be negative.

This tax amount is reflected as the organization's debt, which does not increase the amount payable to the employee. Excessively withheld personal income tax is taken into account when calculating the employee’s wages in the following periods and reduces the amount of calculated tax.

If you need to return the excessively withheld amount of personal income tax, then you should draw up a document “Return of Personal Income Tax”.

In order to draw up this document, you need to go to the “Salaries and Personnel” section and select “All personal income tax documents”. By clicking the “Create” button, we select the document we need, namely “Personal Income Tax Return”.

This document must indicate:

- Date of the document;

- Name of company;

- Month of the tax period in which the tax refund occurs;

- An employee to whom a refund of over-withheld tax is made.

In this case, the tabular part of the document is filled in automatically after the required employee has been selected in the “Employee” field. The date of receipt of income, as well as the amount of tax to be refunded, will be automatically entered.

If necessary, you can update the amounts to be refunded by clicking the “Update refund amounts” button, or you can add amounts manually by clicking the “Add” button.

The document “Personal Income Tax Return” itself does not generate postings in the 1C: Accounting program. With its help, only the amount of tax to be refunded is generated, which will subsequently be reflected in the tax accounting registers for personal income tax.

Let's consider solving the problem of returning personal income tax based on an employee's application.

After studying the material you will learn:

- how to register a personal income tax return to an employee upon his application in the 1C: ZUP 3 program;

- what amount of personal income tax should be transferred to the budget after the tax is refunded to the employee and how to reflect this in the 1C: ZUP 3 program;

- How the amount of personal income tax refund is reflected in the reports: 2-NDFL, 6-NDFL, Tax Registration Register for Personal Income Tax.

Regulatory regulation and stages of personal income tax return

To solve the problem, you first need to consider the regulatory regulation of personal income tax returns. The procedure for returning personal income tax to the taxpayer is described in Art. 231 Tax Code of the Russian Federation.

Stages of personal income tax return:

- excessively withheld personal income tax was detected;

- inform the employee about this within 10 working days;

- the employee must write a statement;

- within 3 months the organization must return personal income tax;

- Personal income tax refunds are made strictly to the employee’s bank account, i.e. You cannot return personal income tax through the cash desk.

Registration of property deduction and recalculation of personal income tax

A property deduction for an employee is registered in the program with a document Notification of non-commercial organizations about the right to deduction (Taxes and contributions – Application for deductions – Notification of non-commercial organizations about the right to deductions).

It states:

When calculating wages for March 2017 in the document Calculation of salaries and contributions Personal income tax is recalculated from the beginning of the year.

On the tab Personal income tax The amounts of actually provided property deduction are reflected in 10,000 rubles. for 3 months and personal income tax for January and February 2017 is recalculated at -1,300 rubles:

On the tab Payment adjustment The amounts of personal income tax to be refunded are reflected:

Using the amounts on this tab, you can track the occurrence of excessively withheld personal income tax, which must be reported to the employee.

Personal income tax refund

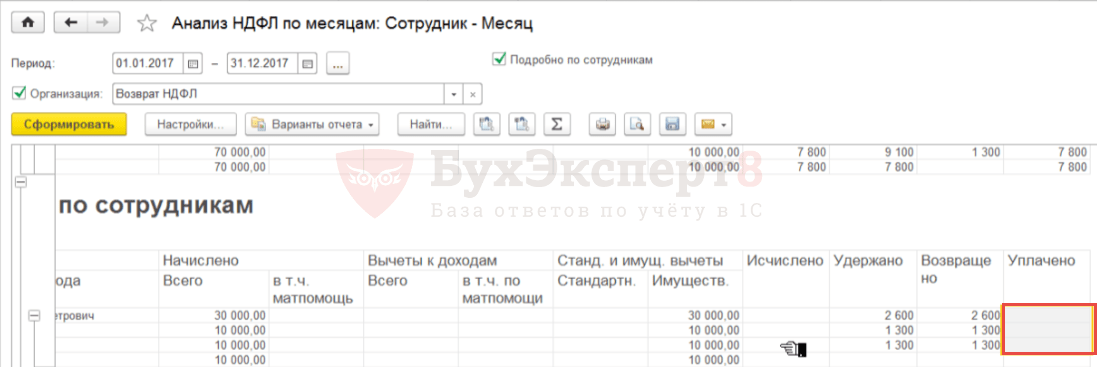

You can check the amount to be refunded using the service Analysis of personal income tax for refund (Salary – Service – Analysis of personal income tax for refund):

To register the personal income tax refund amount, the employee must create a document Personal income tax refund (Taxes and contributions – Personal income tax refund).

In field Month select the month in which the personal income tax refund will be reflected. By button Update refund amounts The amount is automatically loaded - 2,600 rubles. with the date of receipt of income – 02/28/2017:

Payment of the refund may be made along with the payment of wages.

Transfer of personal income tax to the budget in the month of tax refund

In the month when the tax refund occurred, the amount of personal income tax transferred by the organization to the budget is reduced by the amount of the returned personal income tax.

For this purpose in the document Statement to the bank you need to uncheck the box The tax is transferred along with the salary :

As a result, when carrying out Vedomosti Information on amounts paid to the employee and personal income tax withheld will be recorded.

In order to reflect the fact of tax transfer in the program, you need to create a document Transfer of personal income tax to the budget (Taxes and contributions – Personal income tax transfers to the budget).

When posting a document Transfer of personal income tax to the budget in the accumulation register, the negative transfer for the employee for whom the refund was made will be written off, and for other employees, the amounts deducted from them will be registered as transferred:

Clarification of the date of receipt of income in the document “Personal Tax Return”

To check the correctness of the reflection of information on the return of personal income tax and its transfer, you can generate a report Personal income tax analysis by month (Taxes and contributions – Reports on taxes and contributions – Analysis of personal income tax by month) grouped by Employee and Month of the tax period.

In general, the amount of personal income tax paid by the employee is returned by I.P. – zero, but there is a positive and negative amount for January and February, respectively:

It turns out that in the program:

- for January 2017: personal income tax withheld but not returned was recorded. The amount of tax paid remains;

- for February 2017: personal income tax withheld and over-returned was recorded. A negative amount of tax paid appeared.

If necessary to:

- the amount of personal income tax returned corresponded to the amount of tax withheld not only for the period as a whole, but also for each month;

- the amount of personal income tax paid became zero not only for the period as a whole, but also for each month,

then you need to manually correct the information in the document Personal income tax refund , breaking down the total amount to RUB 2,600. (automatically falling in February) for two periods: January and February for 1,300 rubles:

After this, you need to update the tax information in the document Statement to the bank by clicking the corresponding button Update tax .

As a result, in the accumulation register Calculations of tax agents with the personal income tax budget A negative transfer for an employee will be divided into 2 lines - for January and February: